Bridging the gap between words and action in human rights reporting

In recent years, many large companies have made considerable steps towards aligning with global human rights standards such as the UN Guiding Principles on Business and Human Rights (UNGPs) and the OECD Guidelines for Multinational Enterprises on Responsible Business Conduct, while also strengthening sustainability disclosures under frameworks like the EU Corporate Sustainability Reporting Directive (CSRD). Yet, companies may publish detailed sustainability statements that say little about the actual human rights impacts behind those disclosures, and how the company is addressing them.

In many organisations, the processes of human rights due diligence (HRDD) and sustainability reporting remain separate. Reporting teams are busy compiling available information, data and indicators for annual disclosures, while human rights teams focus on identifying and managing risks through more dynamic processes that cannot always be captured in formal reports. The power lies in bringing these two elements together: to move from disclosing what is easy to measure towards meaningful accountability and action.

This blog outlines how HRDD and sustainability reporting could strengthen each other, and what integration of the two means in practice.

Two-sided reinforcement: how HRDD and reporting strengthen each other

Human rights due diligence and sustainability reporting were designed with different purposes in mind, yet they share a common goal: ensuring that companies understand and communicate their impacts on people and the environment transparently, take accountability for them, and follow up responsibly. When performed in close alignment, the two become mutually reinforcing: one providing substance, the other structure.

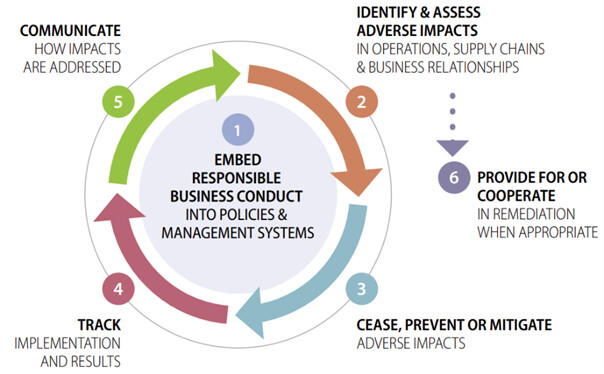

HRDD generates a deep understanding of how business activities affect people, like workers, communities, consumers, and other stakeholders, across the value chain. It involves assessing actual and potential adverse impacts on human rights, integrating findings into decision-making, tracking responses, and communicating progress. This process creates a continuous flow of insights that can anchor sustainability reporting in real-world data rather than abstract commitments, in line with the 6-steps due diligence cycle of the OECD.

[Source: OECD Guidelines for Multinational Enterprises (2023)]

Conversely, sustainability reporting gives HRDD visibility and direction. The European Sustainability Reporting Standards (ESRS) under the CSRD, particularly the social standards (ESRS S1–S4), require disclosures that mirror key HRDD components: governance structures, policies, risk assessment, mitigation actions, targets, and progress. In this way, reporting requirements aim to formalise and institutionalise due diligence efforts by triggering transparency and accountability. They encourage companies to make HRDD more systematic: no longer a project or a workshop, but a documented process embedded in governance and risk management systems, thereby completing the due diligence cycle.

When companies approach these activities as two sides of the same coin, a self-reinforcing cycle emerges. HRDD findings help determine which issues are material under the CSRD’s double materiality lens, ensuring that the sustainability report focuses on what truly matters, namely the most severe (potential) impacts on people and planet. At the same time, the reporting cycle, including collecting evidence, defining metrics, and disclosing results, drives continuous improvement in HRDD practices.

Integration in practice

In practice, this alignment requires cultural and organisational change more than technical tools. It means that, ideally, the HRDD and reporting functions are not two separate teams handing off information, but part of one continuous, collaborative process of understanding and communicating impact. For example, stakeholder engagement through HRDD can directly inform the materiality assessment for reporting. And KPIs developed for reporting can guide follow-up actions to mitigate adverse human rights impacts.

The integration requires companies to rethink what “data” means. Next to quantitative indicators used for reporting, the qualitative information from performing HRDD adds meaningful insights to data-driven disclosures. When combined, these provide a more complete picture of corporate performance. Numbers without context lack meaning, while narratives without structure lack credibility. A well-integrated approach bridges that divide.

Importantly, the feedback loop does not end with disclosure. Transparent communication about human rights impacts invites external scrutiny, from investors, NGOs, and communities. This in turn enriches the next cycle of HRDD. Reporting thus becomes not just a compliance tool, but an accountability mechanism that keeps due diligence grounded in the realities of people affected by business operations.

Several companies have already started to demonstrate this synergy. For instance, Unilever and IKEA embed HRDD insights directly into their annual sustainability disclosures, explaining how risks are prioritised and what outcomes have been achieved. Or Heineken, who links stakeholder engagement findings to its double materiality assessment, ensuring that its reporting reflects real-life risks.

In summary: beyond compliance, towards people-centred accountability

Integrating human rights due diligence processes with general sustainability reporting does more than align with EU requirements like the CSRD and the upcoming Corporate Sustainability Due Diligence Directive (CSDDD). It represents a deeper shift in how companies define accountability.

When HRDD and sustainability reporting reinforce one another, organisations move from box-ticking disclosure to a model of people-centred accountability. They can demonstrate how they understand, prioritise, and address their most significant human rights impacts. Not just for regulators or auditors, but for the people whose rights and livelihoods are affected by their operations.

In this integrated approach, HRDD ensures that reporting is grounded in reality, while reporting ensures that HRDD is transparent and leads to actual accountability. The outcome is more than compliance: it’s credibility. Companies that succeed in merging these practices show that sustainability reporting can be both rigorous and human, and both measurable and meaningful. By connecting insight with accountability and action with transparency, businesses can demonstrate not only what they are doing but also why it matters.

Marco Kwakernaat (consultant sustainability strategy and reporting) and Lisanne Hekman (human rights consultant) from 2impact. Want to know more? Please contact Marco or Lisanne