Market-Based Instruments in Climate Action: Carbon Credits & Book-and-Claim

Market-based instruments (MBIs) are playing an increasingly important role in climate policy and corporate climate strategies. As companies and governments work towards ambitious climate targets, these instruments are used to channel investment into emission reductions and low-carbon technologies.

At the same time, expectations around climate claims are rising. Emission reporting is no longer a tick-box exercise. Investors, regulators and customers increasingly expect climate action to be measurable, verifiable and credible.

Within this landscape, two types of market-based instruments are particularly relevant for companies:

- carbon credits, which are typically used for carbon offsetting, and

- Book-and-Claim systems, which are increasingly used to support carbon insetting and sector-based decarbonisation.

Although both approaches involve tradable certificates representing environmental attributes, they operate in different ways and serve different purposes within corporate climate strategies.

Understanding the difference between these mechanisms is becoming increasingly important as climate accounting frameworks evolve.

Major standards are currently reviewing how market-based instruments should be used in emission reporting. The Science Based Targets initiative (SBTi) is updating its Corporate Net-Zero Standard, and the GHG Protocol is reviewing its guidance on how companies account for purchased environmental attributes.

These discussions reflect a broader question: how can market mechanisms be used to support credible and effective decarbonisation? Central to this conversations are carbon credits that enable companies to invest in emissions avoidance, reductions, or removals outside their own operations and value chain. However, it cannot be used as a mechanism to reduce absolute scope 1, 2, and 3 emissions.

Alongside these, innovative market-based instruments like ‘book and claim’ systems, particularly in areas such as sustainable aviation fuel and freight transportation, are gaining traction as ways to bridge the gap between ambition and action. But what exactly are these mechanisms, and how do they function in practice?

Carbon Credits and Carbon Offsetting

Carbon credits are one of the most widely known market-based instruments. A carbon credit typically represents one tonne of carbon dioxide equivalent (CO₂e) that has been reduced, avoided, or removed through a specific project.

Companies often purchase these credits to offset emissions they cannot yet eliminate. Typical offset projects include reforestation, renewable energy development, methane capture or industrial carbon removal technologies.

Offsetting therefore directs finance to emission-reduction activities outside a company’s own operations or value chain. While carbon credits are widely used for the neutralization of unavoidable emissions, the Science Based Targets initiative (SBTi) clarifies that they should complement, not replace, direct emissions reductions within a company’s value chain. SBTi’s guidance underscores that credible net-zero strategies prioritize cutting emissions at source, reserving high-quality credits solely for neutralizing residual emissions as a final step.

However, the effectiveness of some offset programmes has been widely debated. A review of more than two decades of research found that certain carbon credit systems have overstated climate benefits due to issues such as non-additionality, leakage and over-crediting linked to uncertain baselines.

This does not mean carbon credits cannot contribute to climate mitigation. However, it has led regulators, standard setters and companies to examine more closely how these instruments are used and what claims they support.

Book-and-Claim and Carbon Insetting

Book-and-Claim systems represent another type of market-based instrument.

They are based on a chain-of-custody approach that separates environmental attributes from the physical flow of goods or energy. Instead of tracking a specific product or fuel through a supply chain, the environmental benefit is recorded in a registry and allocated through certificates.

This concept is widely used in electricity markets. When a company purchases a renewable energy certificate (REC), it does not necessarily receive electricity directly from a specific wind or solar installation. Instead, it purchases the environmental attribute associated with renewable electricity generation, which is tracked and retired in a registry.

Book-and-Claim systems apply a similar logic in sectors where low-carbon inputs are difficult to trace physically.

In the maritime sector, for example, the use of sustainable marine fuels can generate verified emission reductions. These reductions are recorded in digital registries and converted into certificates that can be allocated to companies participating in the system.

Importantly, the company making the claim does not need to use the same vessel or fuel supplier. Instead, it supports verified low-carbon activity somewhere within the sector.

This mechanism is increasingly used to enable carbon insetting, where companies invest in emission reductions within their own value chain or sector rather than compensating emissions elsewhere. “While book-and-claim systems offer a flexible way to allocate environmental benefits through certificates rather than physical tracking, they are not yet recognized by standards like SBTi for reducing Scope 1 or Scope 3 emissions, due to concerns about additionality and the risk of double counting.”

Market-Based Instruments in Climate Accounting

As the use of market-based instruments grows, climate accounting frameworks are evolving to clarify how these mechanisms should be used.

Under the GHG Protocol Scope 2 guidance, companies can use renewable energy certificates to account for renewable electricity purchases under the market-based accounting method. However, the guidance is currently under consultation, with proposed updates emphasising closer matching between renewable generation and electricity consumption in both time and location.

The Science Based Targets initiative similarly emphasises that companies should prioritise direct emission reductions within their own operations and value chains. Purchased mitigation instruments may complement these efforts but should not replace internal decarbonisation. Under the GHG Protocol Scope 2 guidance, companies can use renewable energy certificates to account for renewable electricity purchases under the market-based accounting method, while the location-based method reflects the actual grid mix where consumption occurs.

In sectors such as aviation and shipping, where technological solutions are still developing, market-based instruments like Book-and-Claim systems are increasingly being explored as ways to stimulate demand for low-carbon fuels and technologies.

The GHG Protocol (GHGP) is currently considering adjustments to its corporate accounting framework by introducing Actions and Market Instruments (AMI) Guidance, which will expand how companies report and account for emissions reductions, including those achieved through market-based instruments for Scope 1 and Scope 3, in addition to the guidance on scope 2 reporting.

The ongoing AMI public consultation aims to clarify how market-based accounting (e.g., carbon credits, renewable energy certificates) can be integrated with direct physical inventory reporting, ensuring transparency and avoiding double-counting. Stakeholders will help define eligibility criteria, safeguards, and methodological boundaries, such as additionality, leakage, and permanence—to ensure market instruments credibly complement physical emissions reductions in corporate climate strategies

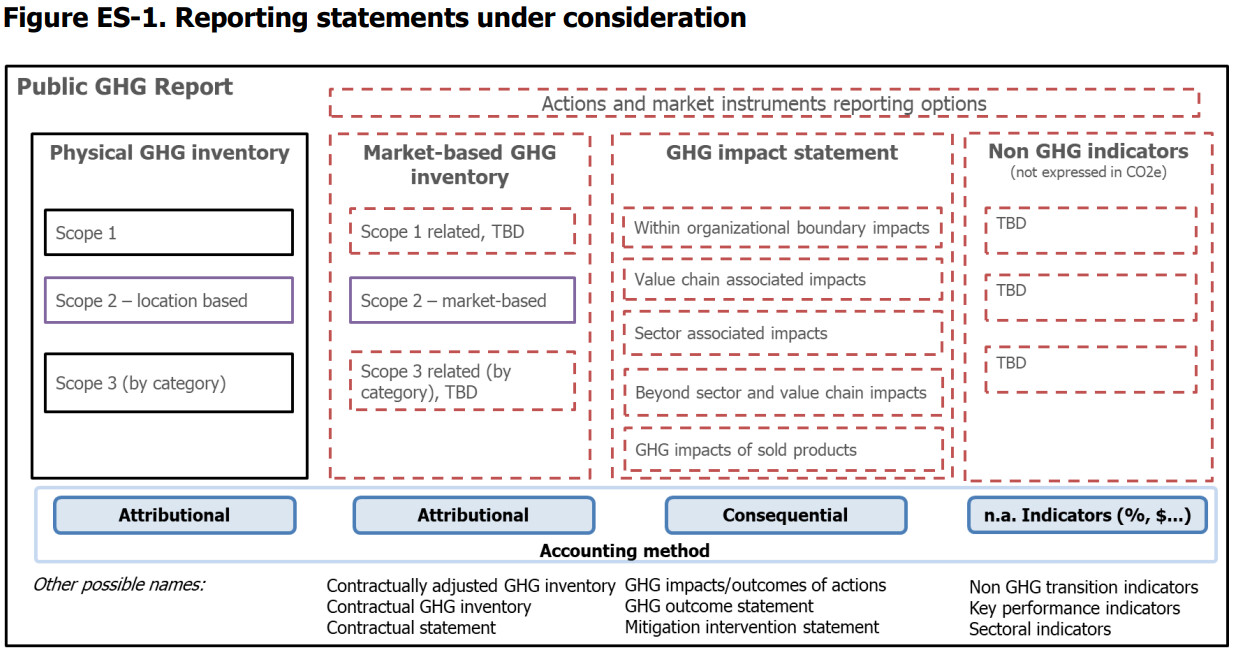

A recent development that further shapes this discussion is the GHG Protocol’s 2026 Actions and Market Instruments (AMI) Phase 1 white paper. The document proposes a shift toward a multi-statement reporting framework, where companies would report not only their physical greenhouse gas emissions, but also separately disclose the impacts of their climate actions and the role of market-based instruments. Under this approach, instruments such as carbon credits, certificates, and Book-and-Claim systems would not be used to adjust a company’s core emissions inventory, but instead reported in distinct statements depending on their nature, either reflecting procurement choices (market-based inventory) or broader climate impacts (impact statement).

The proposed structure is illustrated below, showing how emissions, market-based instruments and climate impacts would be reported in separate statements:

GHG Protocol (2026), Actions and Market Instruments (AMI) Phase 1 Progress Update White Paper (Version 3 - Request for Information).

The paper also introduces a clear distinction between attributional accounting (what a company emits) and consequential accounting (what a company’s actions change in the real world), emphasising that these should not be mixed. Importantly, the framework does not yet define whether or how specific instruments like Book-and-Claim will be accepted, but signals that their use will depend on future criteria around traceability, additionality and robustness.

Strategic Implications for Companies

For companies developing climate strategies, the growing scrutiny of carbon markets highlights the importance of understanding how different instruments function.

Carbon credits and Book-and-Claim systems both rely on certificates representing environmental attributes, but they support different types of climate action.

Carbon credits typically finance emission reductions outside a company’s value chain, while Book-and-Claim systems enable companies to support decarbonisation within their own sectors or supply chains.

In practice, credible climate strategies often combine several approaches:

- Direct emission reductions through operational improvements and low-carbon technologies.

- Sector-based decarbonisation, supported by mechanisms such as Book-and-Claim systems.

- Residual emissions management, potentially using high-integrity carbon removal credits.

For companies with emissions linked to logistics, transport or commodity supply chains, Book-and-Claim systems can play a role in accelerating the deployment of emerging low-carbon solutions.

Conclusion

Market-based instruments will continue to play an important role in climate action. However, different instruments serve different purposes and support different types of climate claims.

Carbon credits are typically used to offset emissions by financing mitigation projects outside a company’s value chain. Book-and-Claim systems, by contrast, allocate verified emission reductions within a sector and can support insetting and sector-wide decarbonisation.

As climate accounting frameworks evolve, understanding how these instruments work—and where they fit within broader decarbonisation strategies, will be essential for companies seeking credible and transparent climate action.