Effective storytelling vs. CSRD compliance – a contradiction?

Let’s face it: reporting under the CSRD requires the current structure of most annual reports to be changed (drastically in some cases).

Why? ESRS requires a separate section in your annual report for ESG information, the so-called sustainability statements, which should be structured into four parts. These parts are: General, Environmental, Social and Governance. For first-time reporters, this is somewhat easier as they can start with a clean slate and follow the ESRS required structure. Companies who have been reporting for years already likely have to restructure their current outline significantly.

How can you ensure your storyline is in place, with all these disclosure requirements coming from the ESRS?

We have been working on this question a lot lately. Many of our clients come to us with this question specifically, as the clock is ticking towards the first officially CSRD compliant reports. While working on these projects, we aim to create a visually appealing, story aligned and CSRD compliant annual report for our clients. In doing so, we came across a few key steps we'd like to share with you:

1. Get inspired

The (obvious) starting point is to have a look at what ESRS requires. Then, we suggest looking into several good practice reports: how do they structure the report, what is located where, how does the design look like, how do they cover the requirements? Scroll through them and see what you do like, and what not.

Some good practices are Orsted, Arla, Akzo Nobel, Scan Global Logistics and BAM.

| Orsted | Structure is ESRS aligned, clear visuals, good presentation of impacts, risks and opportunities, ESRS 2 IRO-2 table (references to disclosure requirements) and Appendix B table (EU datapoints) |

| Arla | Visually attractive, made a distinction between "nice to read" text (white background) and "other ESRS requirements" (grey background), progress table for ESRS disclosure requirements (not mandatory, but interesting to see the progress for each disclosure requirement and how they communicate this) |

| Akzo Nobel | Really tried to incorporate the CSRD structure: the headings refer to the ESRS disclosure requirements so that you can immediately see what the chapter/paragraph is about. |

| Scan Global Logistics | Note – this is a sustainability report, not an annual report. However, for the sustainability statements it provides some inspiration. Especially the presentation of the impacts, risks and opportunities is nice, and they refer to the relevant ESRS disclosure requirements in their report so that you can see what disclosure requirement a certain paragraph covers. |

| BAM | Example of a more integrated structure, where most of the storyline is in chapter 3, and other required information can be found in chapter 6. |

2. Create a high-level overview of your restructured report

Have a look at your current structure. What is already good to go, and which parts need adjustment? Are these big changes or quick wins? What ESRS required information do you want to include by reference (meaning the information will be within the management’s overview) and what will be moved to the sustainability statements? First creating this high-level overview of what information goes where, based on both your current outline and the inspiration you got from point 1, will help you later in the process.

3. Brainstorm sessions: visuals, tables and symbols

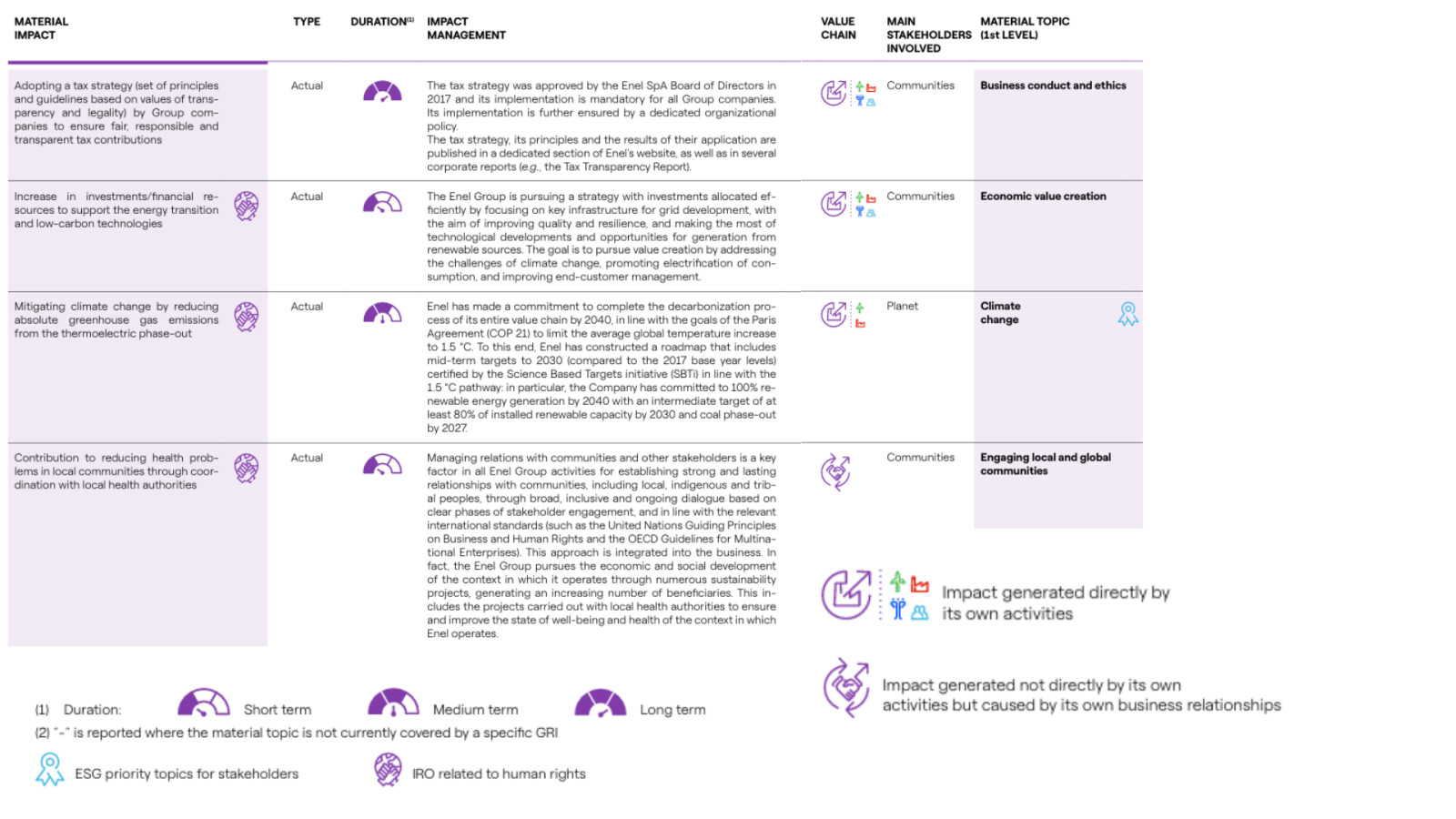

Where do you want to include visuals? What will be the information you want to convey with these visuals? You can think of visuals for the value chain, your strategic pillars, progress charts, IRO tables, etc. Also, where can you include symbols to convey information easier? For example, you could include symbols for where in the value chain a certain impact occurs (see example Enel below).

4. Start with one or two topical standards and work from there

Once you have your high-level overview, you can start with one or two topical standards. For example, how would the E1 - Climate change chapter look like? How can you make sure you cover all the disclosure requirements? You don’t need to include content yet, just think about the structure and the headings. Where can you add visuals? How will you disclose the metrics? How will you include the minimum disclosure requirements? Try to make one or two topical standards, preferably one environmental and one social, as complete as possible. Once you agree on this structure, you can translate it to the other topical standards.

It's worth mentioning that it’s likely that not all topical standards will follow the exact same structure, as the disclosure requirements differ per topical standard. However, starting with really thinking through the structure for one, will help with the others.

Tailor-made approach

To conclude, we see that this restructuring really requires a tailor-made approach. We mentioned some good examples, but we also experience that combining these good practices with the company’s own narrative and current structure into something even better is really the key here.

Curious to know what we can do for you? We host (customized) introduction workshops and working sessions. We are also keen to help you with the overall (re)structuring and even content writing, for example based on your current policies and other internal documents. Feel free to reach out to info@2impact.nl to see what we can do for you.

Link to our service "Sustainability reporting".