VSME – what is the voluntary sustainability reporting standard for SMEs?

VSME – what is the voluntary sustainability reporting standard for SMEs?

With the Omnibus Simplification Package being proposed in February 2025, the rules around sustainability reporting are going through major changes (read more in our blog here). Mid-sized companies—those with 250 to 1,000 employees—were originally expected to start reporting under the Corporate Sustainability Reporting Directive (CSRD) in 2026. However, with the Omnibus and its proposed threshold of 1,000 employees this might change, excluding 80% of companies from the scope of CSRD.

Does this mean companies below the threshold should step back from sustainability reporting? Not really. Expectations from customers, investors, and financial institutions remain strong. These stakeholders still want clear, reliable information on how companies are managing their environmental and social impacts.

This is where the Voluntary Sustainability Reporting Standards for SMEs comes in. The VSME offers a practical path forward for SMEs and businesses that would no longer be legally required to report—but still want to demonstrate transparency, build trust, and stay competitive in an ESG-focused economy.

What is VSME and what is its purpose?

VSME is a voluntary reporting framework tailored for small and medium-sized enterprises (SMEs). Developed by the European Financial Reporting Advisory Group (EFRAG), it offers a simpler, more accessible option for businesses that still want to share their sustainability efforts.

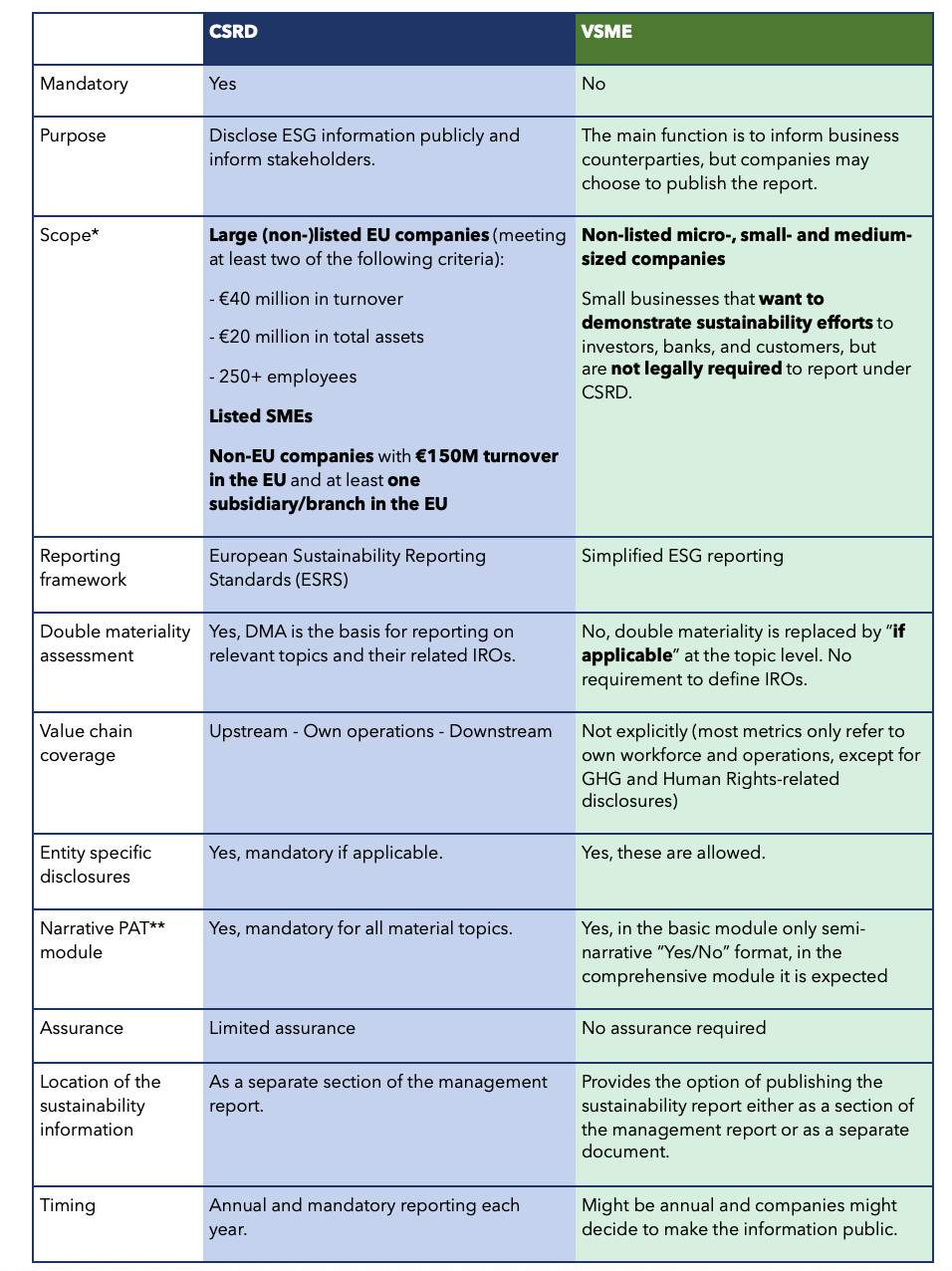

The main difference between CSRD and VSME are summarised as below.

*The scope of the CSRD might change due to future implications of the Omnibus

**PAT stands for policies, actions, and targets

With its lighter and simpler requirements on datapoints, VSME offers a framework to:

- provide ESG information to large undertakings requesting sustainability information from their suppliers;

- provide ESG information that will satisfy data needs from banks and investors, enhancing SMEs' access to finance;

- enhance SMEs' internal sustainability management; and

- transition to a more sustainable and inclusive economy.

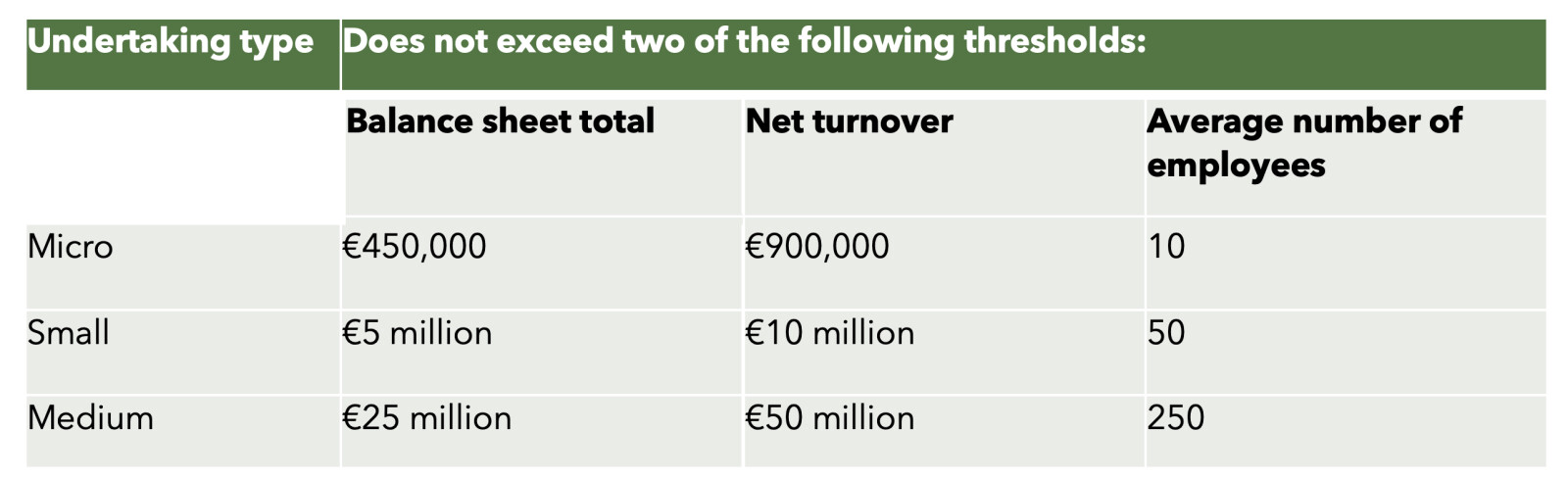

According VSME standard, SMEs are defined as follows:

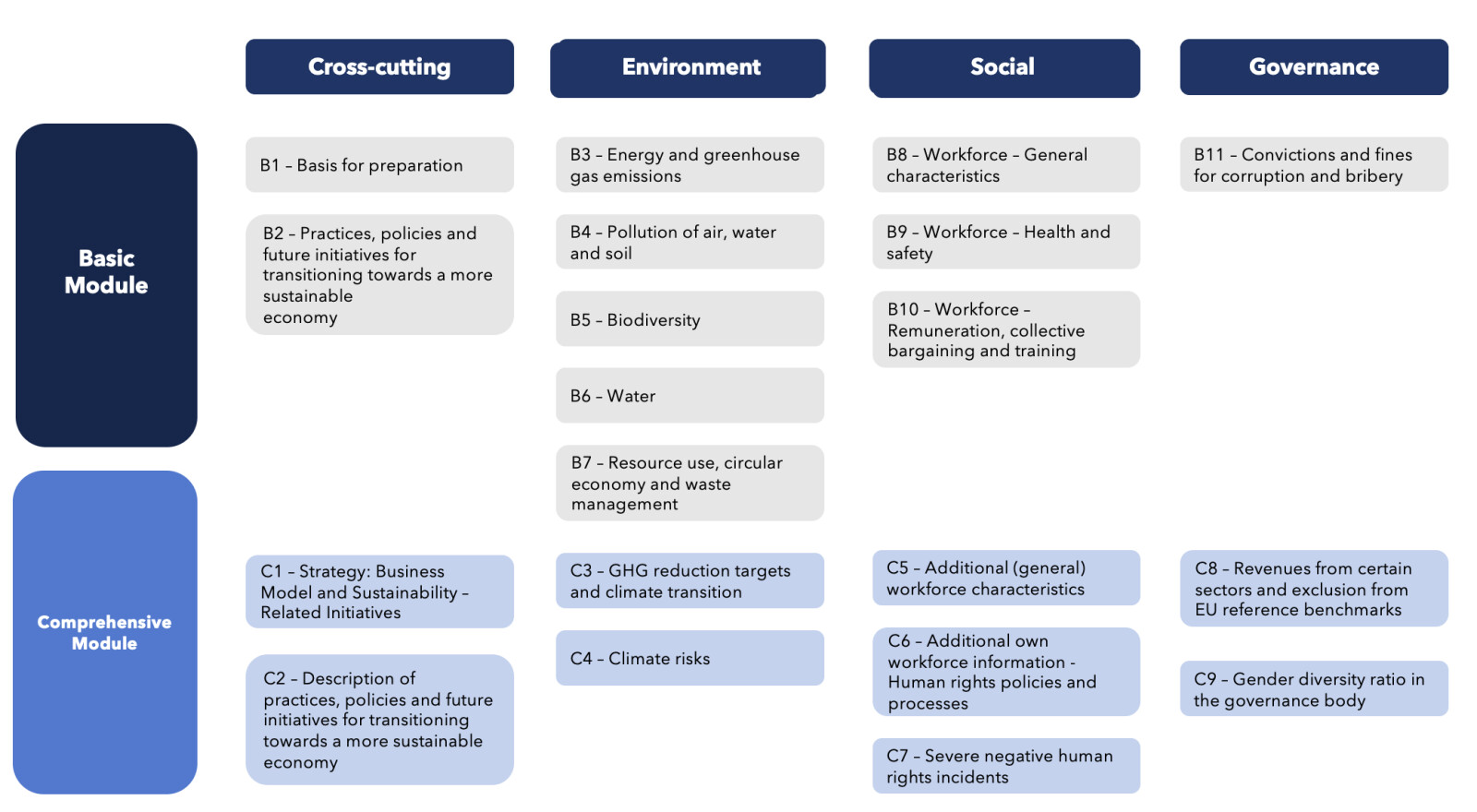

The Basic Module and Comprehensive Module

The VSME framework covers the familiar ESG categories: environmental, social, and governance, and consists of two modules, the Basic Module and the Comprehensive Module. This allows SMEs to choose the level of detail they wish to go into, depending on their needs and the expectations of their stakeholders.

1. Basic Module

The Basic Module consists of 11 disclosures: the cross-cutting disclosures B1 and B2, and Basic Metrics (B3 to B11). The basic module is tailored for micro-undertakings to disclose essential ESG information to meet the requirement from the market and other larger undertakings.

Think of this as the essential snapshot of your sustainability profile. It covers:

- General information: general company information, reporting practices, basic policies, targets and any steps taken toward sustainability transitions.

- Environmental metrics: energy and greenhouse gas emissions, pollution, biodiversity, water, waste, and recourse use.

- Social metrics: workforce breakdown, health and safety, remuneration, collective bargaining, and employee training.

- Governance metrics: anti-corruption and anti-bribery.

2. Comprehensive Module

Adding on the Basic Module, the Comprehensive Module suggests more datapoints, suitable for those who aim to reach a higher disclosure level and report in line with broader requirements from the financial market (e.g. SFDR PAI Table 1, Pillar 3, Benchmark Regulation).

The comprehensive module requires datapoints including:

- Strategy and forward-looking disclosures: including business model and sustainability objectives.

- Advanced environmental metrics: GHG reduction targets and climate transition plan, and climate risks.

- Deeper social topics: additional workforce characteristics, disclosure on labour rights and human rights issues.

- Broader governance details: revenue split by sector, and board diversity indicators.

The "if applicable" principle

While ESRS requires companies to conduct Double Materiality Assessment (DMA) to define material topics, the DMA approach is removed in VSME and is replaced with the ‘if applicable’ principle, meaning that some disclosure requirements can be omitted if the undertaking identifies them as not-applicable to the undertakings' operations, size, and sector.

For example, in B4 – pollution of air, water and soil in the Basic Module, VSME standard says:

“If the undertaking is already required by law or other national regulations to report to competent authorities its emissions of pollutants, or if it voluntarily reports on them according to an Environmental Management System, it shall disclose the pollutants it emits to air, water and soil in its own operations, with the respective amount for each pollutant. If this information is already publicly available, the undertaking may alternatively refer to the document where it is reported, for example, by providing the relevant URL link or embedding a hyperlink. “

If your company is not required by law or voluntarily reports on its pollutants, the disclosure requirement can be omitted.

Which module should I choose?

While the VSME allows companies the flexibility to choose between two modules, we strongly recommend aiming for compliance with the Comprehensive Module. The Basic Module covers only limited information and may not meet the growing expectations for sustainability disclosure from financial markets and other stakeholders.

How to move forward

If your company was previously within the scope of the CSRD and you have started with or done a DMA, we highly recommend including more details about the DMA and basing your sustainability reporting on the outcomes of DMA, even if it is not required by VSME.

Why?

A DMA is a helpful tool in identifying which topics are material and important to your business, serving as a basis for what you report. In the end, the outcomes of a good DMA and an "if applicable" assessment should lead to similar material topics.

In addition, a DMA offers valuable input for developing or updating your ESG strategy, ensuring it reflects the issues that truly matter to your business and stakeholders. This strategy should form the foundation of your sustainability report, guiding the way you communicate your efforts, priorities, and progress.

If you have not done a DMA before, it is worth considering doing it, especially in a simplified form. For example, you might assess the relevance at a sub-topic level instead of doing a deep dive into all relevant impacts, risks, and opportunities. You can also simplify how you score and prioritise topics to keep the process manageable.

In short, while a DMA is not mandatory under the VSME, it can still offer real value by helping you focus your efforts, communicate more clearly with stakeholders, and build a sustainability strategy that fits your company.

Once you have a clear understanding of which topics are material to your business, and know the corresponding disclosure requirements under the VSME, the next step is to perform a gap analysis. This involves identifying which ESG information you already have in place and where gaps still exist.

Based on this analysis, you can develop a roadmap to address the missing elements. Keep in mind that it is entirely possible not all gaps will be filled within the first reporting year. In such cases, it is important to be transparent in your sustainability report about these areas and outline your future plans. For example, indicating that a specific policy will be developed in the coming year.

With your roadmap in place, the final step is to begin drafting your (first) sustainability report. Here are a few tips to support the process:

- Involve colleagues early: Share responsibilities across departments, collaboration makes the workload manageable and improves the quality of insights.

- Create a clear timeline: A well-structured plan or roadmap helps keep the process on track.

- Learn from others: Review reports from peers or recognised best practices in your sector for inspiration and guidance on structure and content.

- Start with what you have: For your first report, do not aim for perfection. Focus on the data and policies already in place and commit to transparency. Remember, reporting is progress.

Start your sustainability reporting journey today

A good DMA can take months to conduct and require regular updates (e.g. annually). If you need help getting started with a DMA, drafting a report aligned with VSME or CSRD, or conducting a gap analysis that brings you a clear view on your ESG strategy, reach out to esther@2impact.nl for a one-on-one discussion. We are happy to hear from you!

Want to learn more? Join our VSME Webinar

Join our 2impact webinar on the 4th of June 2025, where we will break down the essentials of the VSME and guide you with practical examples!